Moving to Czechia in 2026? US Tax Considerations for Americans + Key Updates

- cshepin

.jpg/v1/fill/w_320,h_320/file.jpg)

- 1 day ago

- 3 min read

Czechia (the Czech Republic) has been attracting Americans seeking a high quality of life, vibrant cities such as Prague and Brno, and favorable conditions for remote work and entrepreneurship. But, relocating abroad requires careful attention to U.S. tax obligations, as U.S. citizens and green card holders remain subject to taxation on worldwide income.

This guide outlines the primary tax considerations for Americans moving to Czechia, incorporating the most recent 2026 developments. At Digital CPA US, we specialize in assisting expats and international clients with these complex cross-border issues.

U.S. Tax Filing Obligations Remain in Effect

Relocating to Czechia does not eliminate the requirement to file U.S. federal tax returns. U.S. citizens and resident aliens must generally file Form 1040 if their worldwide gross income meets the applicable thresholds.

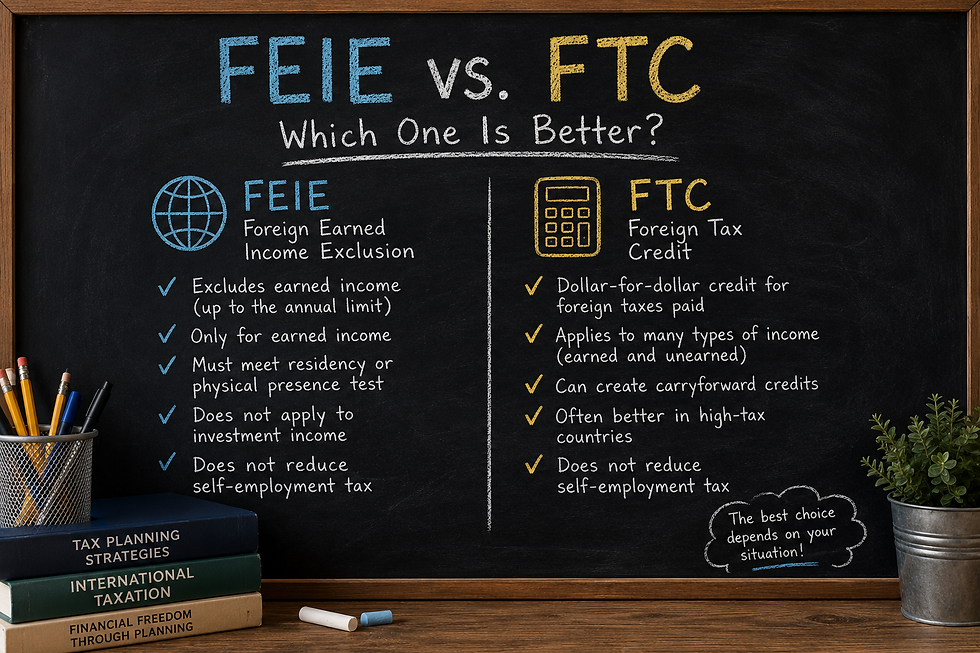

Fortunately, several provisions can significantly reduce or eliminate U.S. tax liability on foreign earnings:

Foreign Earned Income Exclusion (FEIE): For 2026, qualifying individuals may exclude up to approximately $132,900 of foreign-earned income. Eligibility requires meeting either the Physical Presence Test or the Bona Fide Residence Test. This exclusion is claimed on Form 2555.

Foreign Housing Exclusion or Deduction: Additional relief for certain housing expenses abroad.

Foreign Tax Credit (FTC): Offsets U.S. tax liability with taxes paid to Czechia, reported on Form 1116.

Note that the FEIE applies primarily to earned income and should be coordinated carefully with the FTC.

Establishing Czech Tax Residency and Local Obligations

An individual becomes a Czech tax resident if they maintain a permanent home in Czechia with the intention of residing there permanently, or if they are physically present in the country for 183 or more days in a calendar year.

Czech tax residents are subject to tax on worldwide income. Key 2026 personal income tax rates are:

15% on annual gross income up to approximately CZK 1.76 million, (~$76,000–$80,000 USD depending on exchange rate).

23% on income exceeding that threshold.

Social security and health insurance contributions also apply, with withholding typically handled by employers for salaried individuals. Self-employed persons (OSVČ) manage their own contributions and may benefit from simplified flat-rate tax options.

Notable 2026 Developments

Two recent updates are particularly relevant for Americans planning a move:

1. Increased Threshold for the 23% Tax Rate The income threshold for the higher 23% personal income tax rate has risen to approximately CZK 1,762,812 in 2026 (from CZK 1,676,052 in 2025). This adjustment benefits many mid-to-higher earners by allowing a larger portion of income to be taxed at the lower 15% rate.

2. Expanded Digital Nomad Program Czechia’s Digital Nomad Program has been broadened, with eligibility now including U.S. citizens and additional nationalities, as well as marketing specialists alongside IT professionals. The program facilitates long-term visas or residence permits for qualifying remote workers employed by foreign companies or operating their own businesses, often with expedited processing. This option is well-suited for Americans pursuing remote or location-independent work.

Additional changes include updated processing timelines for Employee Cards and new considerations regarding repeated administrative offenses and residence permits.

The U.S.-Czech Tax Treaty and Double Taxation Relief

Moving to Czechia offers an appealing lifestyle, but U.S. citizens and green card holders must navigate ongoing worldwide taxation while complying with Czech rules. The U.S.-Czech income tax treaty and Totalization Agreement provide important relief, helping to prevent double taxation and dual Social Security contributions.

Additional U.S. Reporting Requirements

Americans in Czechia should remain mindful of:

FBAR (FinCEN Form 114): Reporting of foreign financial accounts exceeding $10,000 in aggregate value.

Form 8938: Disclosure of specified foreign financial assets.

Potential requirements for foreign entities, trusts, or other investments.

State tax obligations may also persist depending on prior residency.

Practical Planning Recommendations

Time your relocation strategically relative to tax years and qualifying tests for exclusions.

Maintain detailed records of travel days, expenses, and foreign taxes paid.

Evaluate business structures carefully if self-employed or operating internationally.

Consider professional guidance early to optimize compliance and planning.

Partner with an Experienced Advisor

Navigating U.S. and Czech tax requirements when moving abroad demands specialized expertise. As a CPA with extensive experience supporting Americans living and working internationally, I provide tailored guidance to ensure compliance and strategic tax planning.

Schedule a confidential tax strategy session at digitalcpaus.com/book-online.

This article is provided for informational purposes only and does not constitute tax, legal, or professional advice. Tax rules are subject to change. Please consult a qualified advisor regarding your specific circumstances. Information current as of June 2026.

Comments